As a modern society, we take for granted our current notion of money and how it works. But the concept of money is actually quite malleable and has gone through many notable shifts as we have innovated on financial and payments systems. For example, the proliferation of digital banking has created ease of access for some, but also completely restricted access to those who rely on cash or cannot open a bank account. The wave of digital asset innovation in the past 10 years has also shifted many different aspects of money and what it can do in new and important ways.

Ultimately, money is a very specific form of asset ledger that serves as a means of payment. The money ledger is foundational to a capitalist financial system as the unit of account that everything in the economy is denominated against and from which intertemporal decisions are made. It is also the means of payment for nearly every type of transaction within the economy. Small shifts in how money works can therefore have large implications. Gold, fiat money and cryptocurrencies (e.g. Bitcoin) are examples of ledger systems with different embedded features and technological capabilities. These features distinguish how we use those systems and what possibilities they enable.

It is worthwhile dissecting the empirical attributes of money so we can understand what makes various forms so fundamentally different from each other – and so we can try to move toward a more optimal construct given the many new possibilities technology is now enabling.

Below are the five most important attributes for money ledgers and the most common expressions of these traits.

- Anonymity—The degree to which a third party or central administrator can track identity and transaction details on the ledger

- Anonymous: no direct link between a person’s identity and a transaction (e.g. gold, some crypto currencies like Monero, Zcash, physical fiat cash)

- Pseudonymous: transactions are not linked to a person or identity; however, all transactions are publicly accessible (e.g. Bitcoin, Ethereum)

- Traceable: direct link between a person’s identity and a transaction (e.g. Central bank settlement or reserve accounts)

- Centralization—The concentration of control over the ledger

- Centralized: a single entity controls the ledger (e.g. Central bank, Treasury, Libra)

- Decentralized: multiple participants have the ability to edit the ledger (e.g. gold, Bitcoin)

- Openness—How much access there is to the ledger

- Open: peer-to-peer so anyone can access the ledger (e.g. Bitcoin, gold, physical fiat cash)

- Closed: restricted to members (e.g. central bank money via commercial banks, Libra)

- Limit of Supply—How readily can the quantity of the ledger change

- Constrained, either programmatically or by nature (e.g. Bitcoin, gold)

- Unconstrained: more can always be created (e.g. all central bank money including physical and digital)

- Physicality—Whether the ledger system is natively in a material or dematerialized form

- Digital: meaning the ledger or subledger is fully dematerialized (e.g. commercial bank money, Bitcoin, Libra)

- Physical: existence in tangible form (e.g. gold, physical cash)

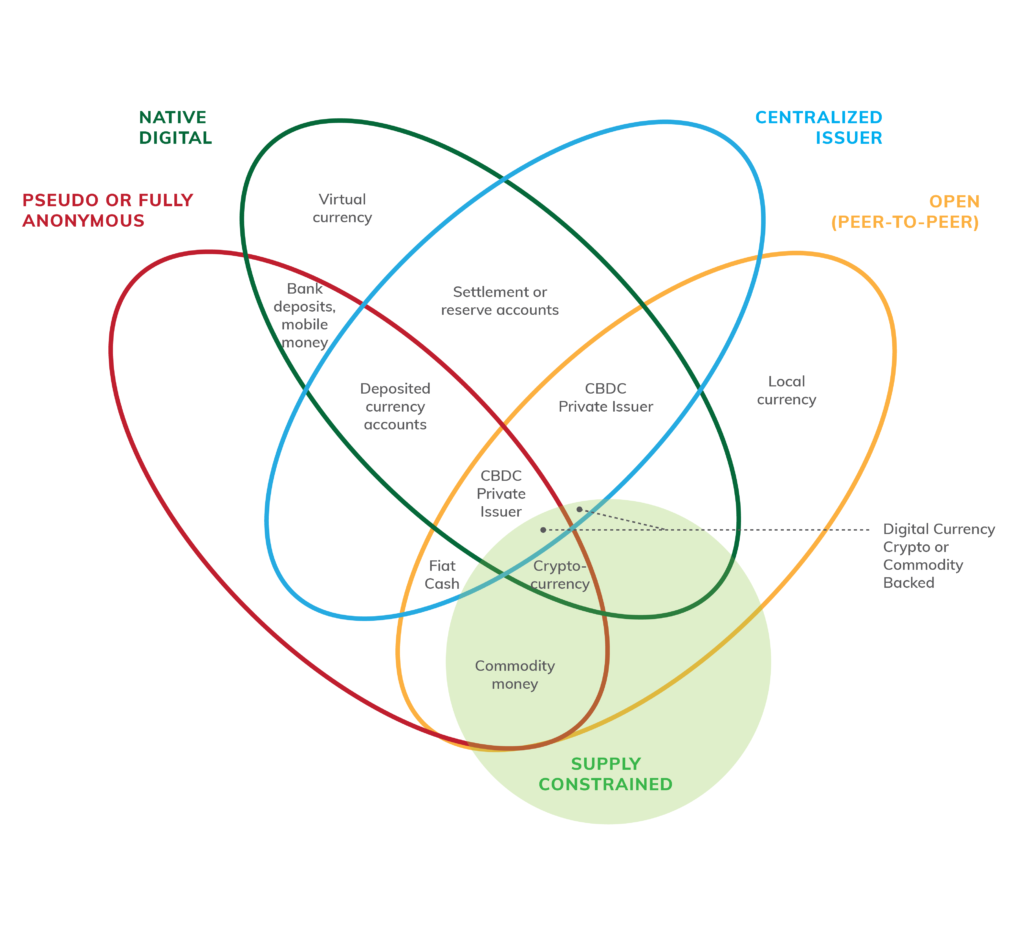

Image 1: The Five Attributes of Money – Visualized

With this taxonomy in mind, it is possible to better understand some of the most common money ledgers and how they compare to each other.

Applied to physical dollars, this theory describes physical dollars as inherently private, centralized, open, unconstrained and physical. Digital banking and electronic payments added the convenience of digital ledgers, but simultaneously decreased privacy and constrained access. The stablecoins we designed at Paxos maintain the privacy and open access of physical dollars, while decentralizing the ledger to allow greater access to it and reduce dependencies on central intermediaries.

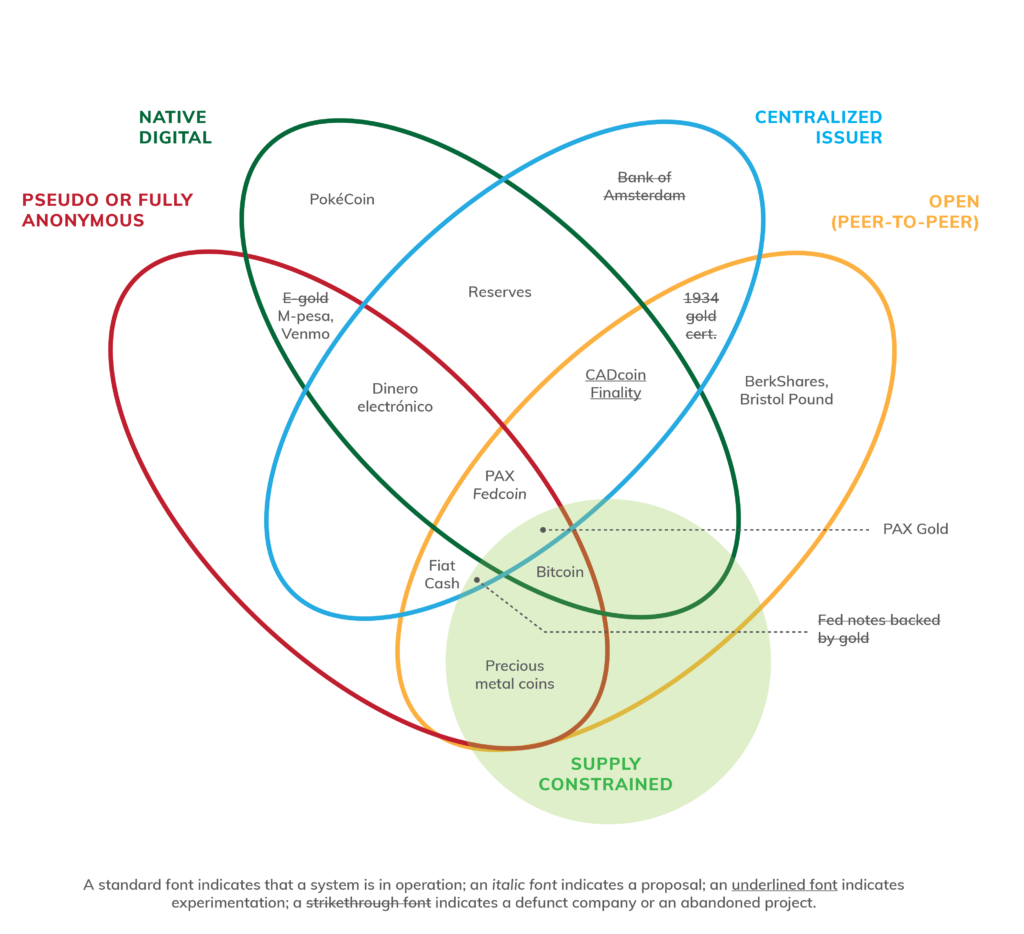

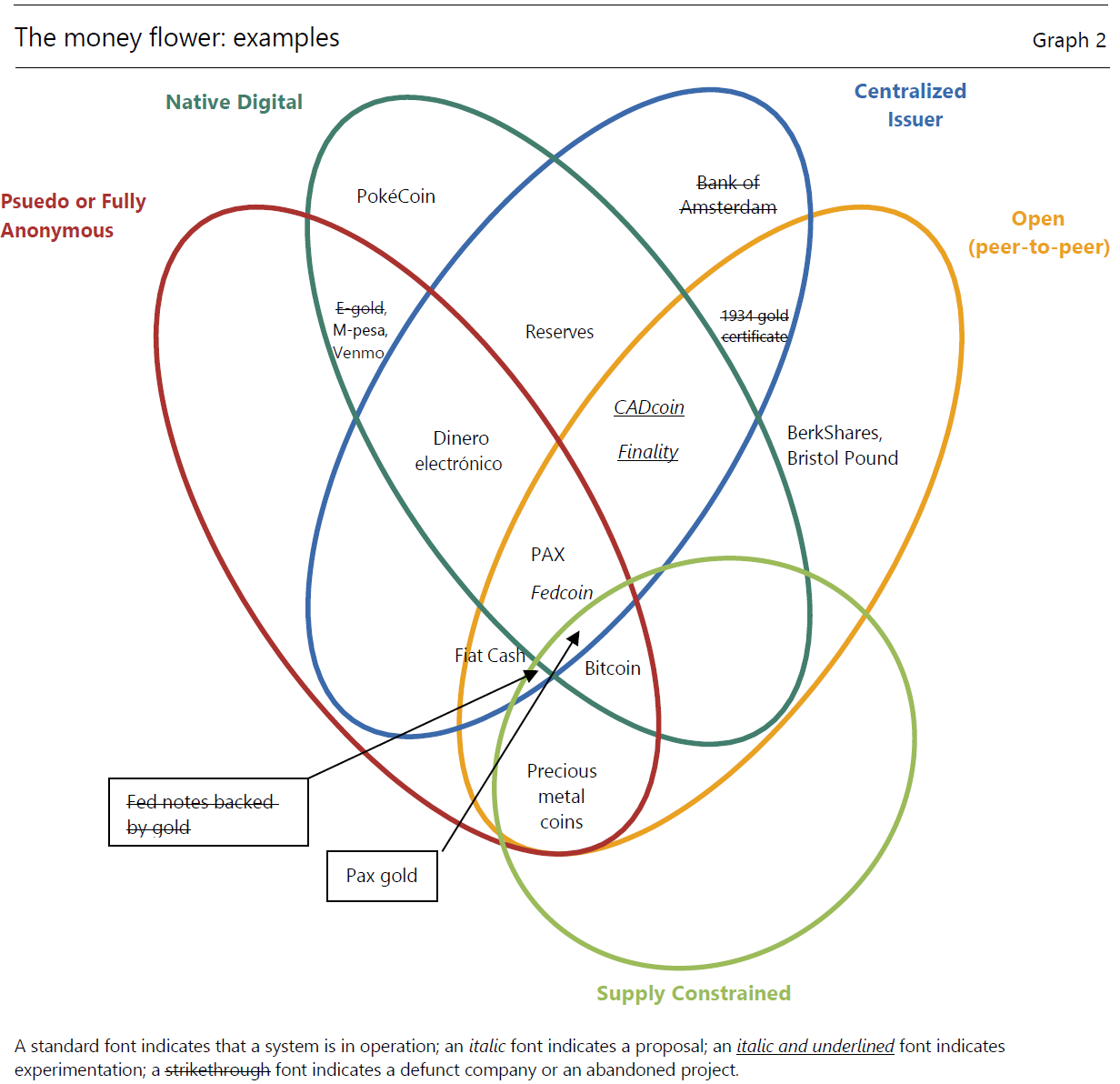

This next version of the “money flower” shows examples of money that has taken on different attributes, including current and past systems that have been created.

Image 2: The Five Attributes of Money – Examples

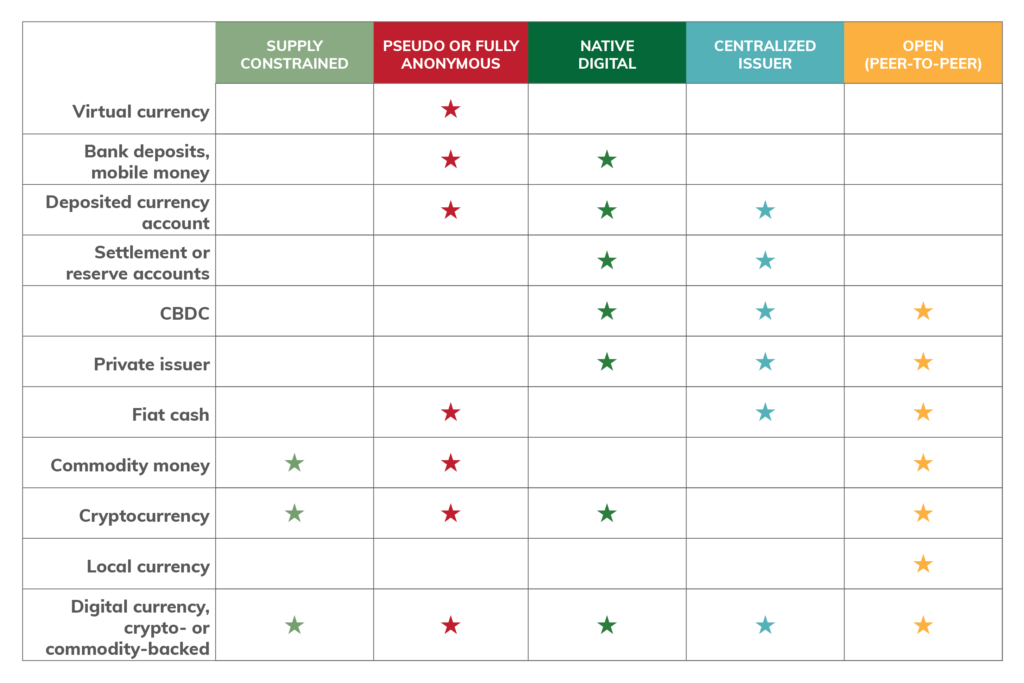

Finally, here is a chart that compares the various attributes and examples.

This construct helps us to dissect how various forms of money ledgers differ and the transformation of money over time. Importantly, this foundation also allows us to examine some important implications and hypothesize on the future—stay tuned for the next piece in this series.

Historically Common Model: Open, Decentralized, Anonymous, Supply Constrained Money Ledgers

Currently, fiat money is generally centralized, traceable and unconstrained, but this is a relatively recent phenomenon (starting in 1971). However, historically, money was open, decentralized, anonymous and supply constrained and there is clearly important utility to this combination of attributes.

Gold is the most ubiquitous commodity money and is fully anonymous, decentralized, open, supply constrained and physical. While gold is still used as money, its primary function is store of value. Historically used as money, it has been hampered in recent times from its physical nature which creates serious limitations in a global and digital world. Importantly, gold is only currently supplied constrained—it grows by the amount mined on Earth each year (~2%). However, gold is only scarce on the surface of the Earth. Whereas it is far more common in the solar system and in the foreseeable future mankind may access these broader supplies of gold. For example, one small asteroid could easily contain a very meaningful percentage of the existing gold stock which would be problematic in maintaining a supply constrained ledger as a store of value.

Cryptocurrency (e.g. Bitcoin) is pseudo-anonymous, decentralized, open, supply constrained and natively digital. Bitcoin is the first cryptocurrency and the best proxy to use as it ranks highest in nearly every important metric including market cap, transaction volume and developer engagement. Its invention created a money ledger very similar to gold with two crucial differences: Firstly, and most importantly, it is natively digital and therefore created an open, decentralized ledger that did not have to exist in physical form. Secondly, it is verifiably supply constrained with a programmatic cap at 21 million Bitcoin, subject to a majority of the network changing the rules. This is inherently deflationary and has no prior antecedent in a successful money ledger and many other cryptocurrencies have opted for some form of a programmatic perpetual inflation.

Today’s Dominant Model: Centralized Money Ledgers

Today, centralized money ledgers are managed by governments, either directly or, more commonly, by central banks acting as their agents. The common feature of these systems is their centralized nature and the control it gives a privileged actor to earn seigniorage (profit from issuing currency), to control access to the system and to create variable scarcity. For example, in the U.S. this authority is largely delegated to the Federal Reserve, though the U.S. Treasury issues fiat coins through its agency, the U.S. Mint.

As the centralized currency issuer, the Federal Reserve has various liabilities with different features ranging from physical Federal Reserve Notes (fiat cash) to purely digital Fed Funds Reserve Balances and Deposit balances. The money flower does a good job mapping the different types of centralized money ledgers, but omits a key feature: supply constraint. Given the contentious nature of Quantitative Easing and central bank balance sheet expansion, the omission is perhaps unsurprising, but supply constraint (through gold backing) has historically been a feature of central bank ledgers.

Below is a closer look at some of the centralized systems mapped in the money flower:

- Physical federal reserve notes (paper, not coins) are anonymous, centralized, open, unconstrained and physical. This is the best analogue to a potential “Fedcoin,” or centralized bank digital currency (CBDC), as it would share all of the same characteristics as physical money, but would be natively digital.

- Federal Funds Reserve Balances and Deposit Balances are traceable, centralized, closed, unconstrained and digital. Accessible only to Federal Reserve Members such as banks and government organizations, these balances sit in a closed system. Digital U.S. dollars in this system must be held in a banking institution with various networks (e.g., Visa/MasterCard/ACH/TCH/CLS) that facilitate cash movement between banks or within the Federal Reserve.

- Central Bank Digital Currency (CBDC) is traceable*, centralized, closed*, unconstrained*, and digital. There are many design options for a CBDC, each proposing different degrees of anonymity and openness. In the future, supply constraint may become a necessary factor in maintaining CBDC credibility, but this is not a concern today.

Some CBDC design options differ only marginally from current Fed liabilities. For example, commercial bank members could still be used as distribution agents for the broader public, but they could allow anyone to then hold and transfer cash. Some smaller countries such as Cambodia are experimenting with such a model, as is China, purportedly.

On the other end of the CBDB spectrum would be a nearly open and pseudo-anonymous CBDC. Such a system would allow peer-to-peer movement of dollars and could permit non-bank institutions to access the central bank directly. (This would certainly have banking policy implications as it would diminish the role of banks as intermediaries.) This type of CBDC would have very similar characteristics to fiat cash and USD stablecoins such as PAX (see below).

Paxos USD (PAX) stablecoin is a privately intermediated version of a CBDC that is pseudo anonymous, centralized, open, unconstrained and digital. Paxos takes USD deposits from customers that have been onboarded with bank-level AML/KYC and issues a regulated stablecoin. Each stablecoin is backed one-for-one with segregated U.S. dollars held bankruptcy-remote in t-bills or with FDIC insurance, so there is limited commercial bank risk. The stablecoin resides on an open blockchain, which is accessible to anyone.