Best Execution in Crypto: It's Time to Raise the Bar

This is the second in a series on how Paxos is building institutional-grade brokerage infrastructure. In our first post, we introduced upgraded multi-venue order routing. Here, we go deeper on what best execution actually means in crypto and how to measure it.

The execution standard crypto hasn't built, yet

For years, "execution" in crypto meant connecting to an exchange, hitting the top of the book, and passing the fill through. Few asked whether the client got the best available price and even fewer benchmarked slippage against a credible reference price. The infrastructure to answer those questions never got built, because there was no obligation to build it.

That's changing fast and in some jurisdictions it's already changed. In the EU, MiCA requires Crypto Asset Service Providers (CASP) to take all sufficient steps to achieve best execution for their clients. In force now, not on the horizon. In the US, FINRA treats best execution as an "evergreen" compliance priority, and the SEC's proposed Regulation Best Execution would extend that obligation further. Regardless of jurisdiction, the question we hear from institutions entering the market has shifted: not "can you connect us to liquidity?" but "can you help us prove we got the best price and show a regulator exactly how?" Crypto doesn't just need to meet that standard. It has the opportunity to exceed it.

Why crypto can do better

Traditional best execution was built around constraints. Equities have consolidated tapes and National Best Bid and Offer (NBBO), but the infrastructure was designed decades ago and carries legacy complexity: fragmented data feeds, opaque routing incentives and quarterly Transaction Cost Analysis (TCA) reports that arrive long after the trades they measure.

Crypto starts from a different place. Yes, liquidity is fragmented across exchanges, OTC desks and market makers, with no consolidated tape or national best bid. However, because the infrastructure is being built now, we have the opportunity to design execution quality from the start. That means real-time analytics instead of backward-looking quarterly reports. It means routing intelligence that improves continuously based on what the data shows. And it means full auditability baked into the execution layer, not assembled after the fact from disconnected logs.

The institutions entering crypto are being held to a TradFi standard. We think they deserve better-than-TradFi infrastructure to meet it.

Measuring what matters, starting with the right benchmark

You can't measure execution quality without a credible reference price. In equities, that's straightforward, NBBO provides a nationally consolidated benchmark. In crypto, no such thing exists. Price discovery happens simultaneously across disconnected venues, each with different depth, fee structures, and latency profiles.

This is one of the most underappreciated problems in crypto execution. If you benchmark your fills against your own internal price, you're grading your own homework. If you use a single exchange as the reference, you're anchored to one venue's liquidity conditions, which may not reflect the broader market.

Our approach: we work with each of our customers to agree on a benchmark, typically an aggregated mid-price constructed from multiple exchanges, and source pricing through independent third-party feeds rather than our own order flow. This matters. Using an external, multi-venue reference price means the measurement isn't biased by the same liquidity pool that filled the order. It's the difference between a self-assessment and an independent audit.

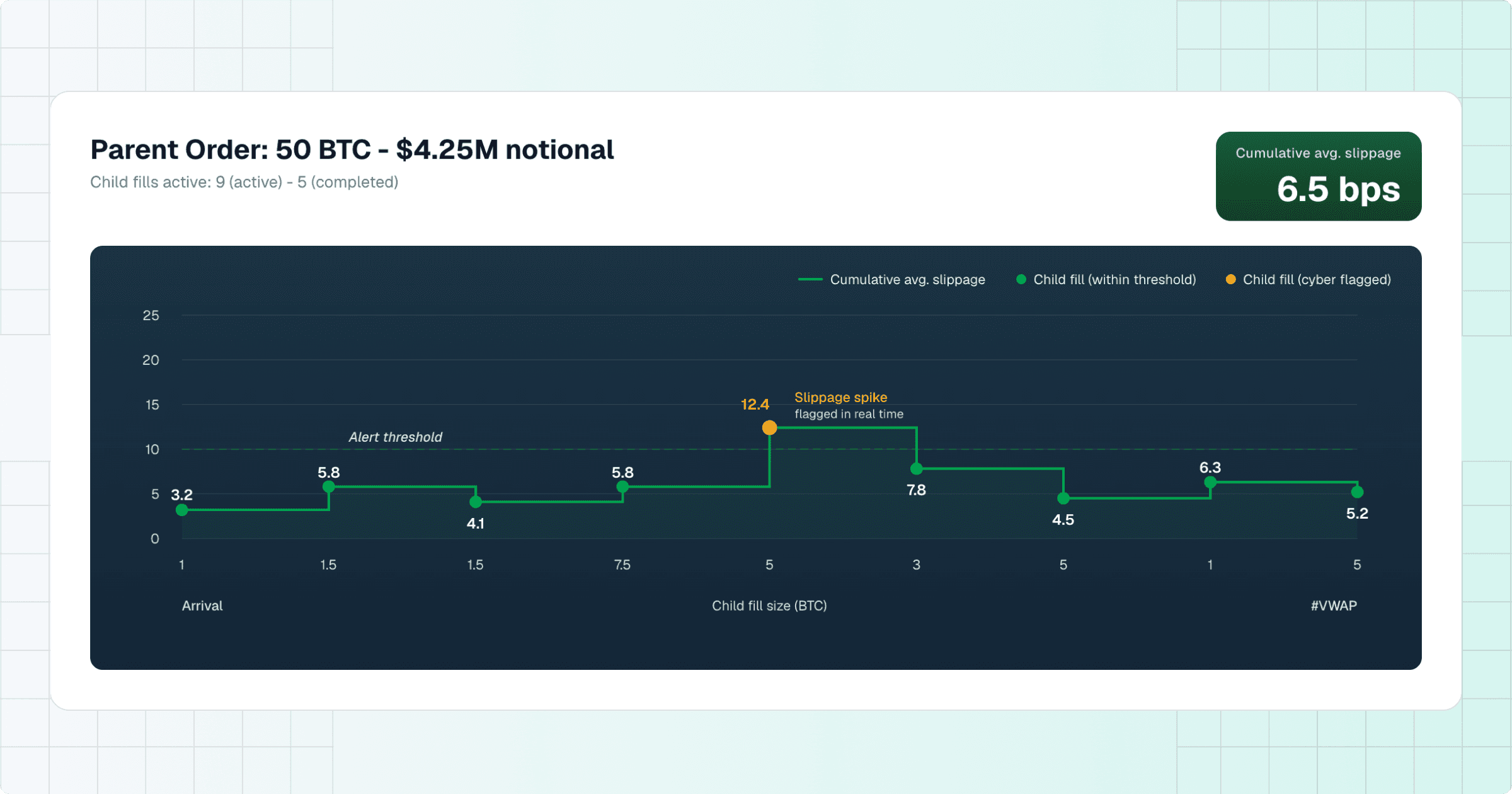

With the benchmark established, we measure what institutional clients and their compliance teams actually need to see: slippage versus arrival mid across different order sizes, because a $10,000 order and a $1 million order live in completely different liquidity environments. We track fill rates, effective spreads, and how the state of the market at the moment of order arrival compared to the state at execution, reconstructing the full picture of what happened and why.

For large parent orders worked across multiple venues and price levels, we also track slippage dynamically in real time as the order executes. Execution quality on a large order isn't determined by the first fill. It can deteriorate across child fills if conditions shift, and catching that as it happens is fundamentally different from discovering it in a post-trade report

From measurement to product improvement

These aren't vanity metrics. They feed directly back into how we improve the product. When our analytics surface a pattern — a particular asset consistently showing higher slippage above a certain order size, or a specific time window where liquidity thins out — that insight informs how the router allocates the next order. Measurement drives product improvement. Better routing produces better measurement. It's a feedback loop, and the more order flow that runs through it, the sharper the system gets.

Monitoring the liquidity, not just the routing

Most execution quality conversations stop at the router. We think that's a mistake. The router is only as good as the liquidity it draws from, and that liquidity isn't static. Market makers quote differently depending on the asset, the session, the volatility regime. Their depth at top-of-book fluctuates. Their rejection rates and quote responsiveness vary. If you're not monitoring the quality of the liquidity flowing into your system, you're flying blind.

We track our liquidity partners across the dimensions that actually matter for client outcomes: fill and rejection rates per provider, how much depth each source contributes at various levels away from mid, how quickly quotes update after market moves, and how concentrated volume is across sources. If depth is thin because a single provider is carrying the book, that's a risk signal. If a provider's quotes are consistently stale by the time orders arrive, that degrades execution quality regardless of how smart the routing logic is.

This monitoring serves two purposes. First, it protects partners: we can identify when a liquidity source is underperforming and adjust routing allocations before it shows up in client fills. Second, it drives the right conversations with our trading counterparts. Armed with data, we can work with liquidity providers to improve their quoting behavior, tighten spreads, or increase depth in specific markets. The result is a liquidity network that gets better over time, not just bigger.

A foundation, not a finish line

We already offer execution analytics and are building toward deeper benchmarking, richer time-horizon analysis, and tools that help partners systematically identify where execution quality is strengthening and where there's room to improve.

What we're most excited about is not the analytics themselves, but what they enable: an infrastructure partner that gets measurably better at execution with every order that flows through the platform and that can prove it.

Every order through Paxos gets multi-venue smart routing, independent benchmarking, and a full audit trail by default. If your firm is looking for an infrastructure partner that can prove execution quality, not just claim it, we're ready to power your next trade. Reach out to your Paxos account team or contact us here.

This is the second in a series of posts about how we're building institutional-grade brokerage infrastructure. Previously: Paxos Upgrades Order Routing to Power the Next Generation of Crypto Brokerage. Next: A closer look at our execution analytics and what they're revealing about crypto market quality.