The Six Layers of Stablecoin Payment Infrastructure

For enterprise fintechs and financial institutions evaluating stablecoin payment infrastructure

Every major fintech is trying to add stablecoins to its payment stack. Most of them are underestimating the problem by an order of magnitude.

The assumption is that stablecoin payments are a product decision: pick a token, add a wallet, wire up an API. In reality, they're an infrastructure decision, one that touches licensing, identity, custody, settlement, conversion, and distribution simultaneously. Miss any single layer and the whole program stalls.

This matters now because the window for treating stablecoins as experimental is closing. Volume crossed $30 trillion. Stripe accepts stablecoin payments for merchants. PayPal offers PYUSD to millions of customers across 70 countries. Consumer-to-business stablecoin transactions more than doubled last year. The infrastructure question has shifted from "should we?" to "how fast can we go live?" and the answer depends entirely on how many layers you have to build from scratch.

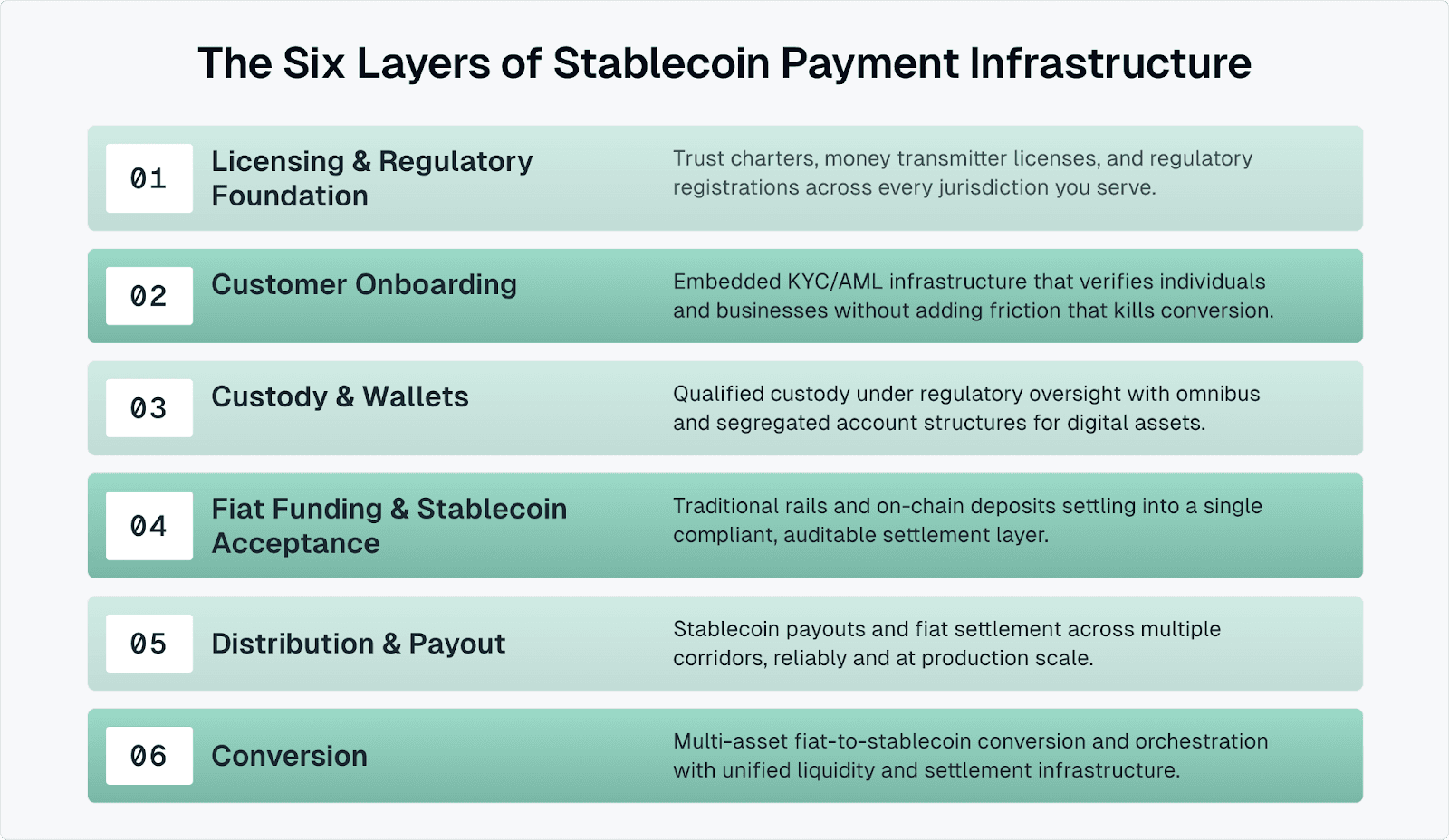

The industry is converging on a six-layer model for stablecoin payment infrastructure. Each layer has its own regulatory surface area, operational complexity, and integration burden. The hardest part isn't any individual layer, it's the connective tissue between them: transaction monitoring, travel rule compliance, sanctions screening, settlement reconciliation, and orchestration logic that has to work across all six simultaneously.

Most platforms trying to solve this end up stitching together point solutions from a dozen vendors, each with its own compliance model and settlement cycle. The result is a system that's technically functional but operationally fragile, and a nightmare to audit.

Paxos built all six layers under a single platform, operated under active regulatory supervision across the US, EU, and Singapore. One integration. One regulated counterparty. Payments companies like Modern Treasury, BVNK, and Confirmo already run their stablecoin flows on Paxos infrastructure.

Here's what each layer actually requires and why a gap in any one of them cascades through the rest.

Layer 1: Licensing and Regulatory Foundation

Every stablecoin payment program starts here, and most stall here.

The regulatory positioning of stablecoin infrastructure providers has become the defining competitive variable in the space. The passage of the GENIUS Act triggered a scramble among issuers and infrastructure companies to secure OCC National Trust Charters, not just for legitimacy, but because charter holders may eventually gain direct access to Federal Reserve rails. Where you sit in the regulatory hierarchy today determines where you sit in the payment hierarchy tomorrow.

For fintechs, the practical implication is stark. Operating across jurisdictions means securing trust charters, money transmitter licenses, or equivalent regulatory registrations in every market you serve. Building that independently takes years of legal work, millions in capital, and ongoing examination cycles. Most fintechs don't have the runway. And the longer they wait, the more the regulatory bar rises.

This is the layer where the build-versus-partner decision gets made, because it's where the cost of building independently is highest and the timeline is longest.

Paxos Trust Company holds an OCC National Trust Charter. That’s bank-level federal regulation providing a single framework for compliant stablecoin operations across the US. Paxos also holds active licenses under MAS (Singapore), and FIN-FSA (EU, MiCA-approved). Partners operate under Paxos licenses instead of building their own regulatory programs, which means compliance and legal teams get a regulated counterparty with over a decade of track record and active supervisory relationships they can reference directly.

Layer 2: Customer Onboarding

Licensing without onboarding is a charter sitting on a shelf. The second layer is where regulatory obligations meet product experience and where most stablecoin programs first discover the tension between compliance and conversion.

Stablecoin programs need KYC for individuals and KYB for businesses. The challenge isn't performing identity verification. The challenge is performing it without adding enough friction to kill the partner's conversion rate. Every additional screen, every document upload, every "pending review" status is a drop-off point. But cutting corners on identity verification creates downstream problems that are far more expensive: blocked transactions, frozen accounts, regulatory enforcement actions.

The UX question is whether onboarding can run as an invisible compliance layer. Ideally something that happens behind the scenes while the end customer interacts only with the partner's product.

Paxos provides embedded KYB/AML infrastructure that plugs directly into partner platforms. Partners who already collect identity data can leverage reliance frameworks to avoid duplicating verification. Paxos also supports silent onboarding, where compliance runs in the background and the partner's customers never interact with Paxos at all. In every model, Paxos remains the regulated counterparty.

Layer 3: Custody and Wallets

Once customers are onboarded and funds are in motion, someone has to hold them. The custody model a platform chooses determines its risk exposure, insurance posture, and fiduciary obligations. This is the layer that enterprise compliance teams scrutinize first.

The distinction between technology-only custody and qualified custody matters more than most engineering teams realize. A technology provider can store digital assets. A qualified custodian holds them under a specific regulatory framework, with examination cycles, capital requirements, and fiduciary duties that technology-only providers don't carry. When an enterprise partner evaluates counterparty risk, or when their regulator does, that distinction is the first thing they check.

This layer also determines what happens when something goes wrong. Qualified custody under a federal charter provides a clear legal framework for asset recovery, claims priority, and regulatory recourse. Technology-only custody does not.

Paxos is one of the longest-standing qualified custodians in digital assets, operating under OCC oversight with SOC 1 Type II and SOC 2 Type II certification. Paxos provides qualified custody with both omnibus and segregated account structures, covering settlement accounts, stablecoin reserves, and multi-asset portfolios under unified regulatory oversight. For digital assets beyond fiat-backed stablecoins, Paxos offers embedded wallet and MPC infrastructure through Fordefi, acquired in November 2025.

Layer 4: Fiat Funding and Stablecoin Acceptance

The first three layers establish the regulatory and operational foundation. Layer 4 is where money actually enters the system and where two fundamentally different technical problems have to converge into a single settlement experience.

On the fiat side, stablecoin programs need to accept real-time payments, wires, and cards. On the crypto side, they need to accept stablecoin deposits directly. Think of a consumer paying a merchant, an enterprise settling into a stablecoin position, a treasury operation funding a wallet. Regardless of how funds arrive, they need to settle quickly and reconcile cleanly under regulated infrastructure. A platform that solves fiat ingress but not stablecoin acceptance (or vice versa) has half an on-ramp and no usable product.

This is the layer where the "bank connectivity" problem arises. Stablecoin infrastructure has been built almost entirely outside traditional banking. Integrating it with legacy core systems requires a dedicated translation layer. When building that layer is where many programs discover that their custody provider doesn't talk to their fiat rails provider, which doesn't talk to their compliance engine.

Paxos provides fiat gateways and regulated settlement accounts that accept traditional rails alongside on-chain stablecoin deposits. Both paths settle into Paxos' trusted infrastructure in a compliant, auditable structure from the moment funds arrive. For companies like Stripe, this means stablecoin payments from consumers can be accepted, converted, and settled to merchants entirely through Paxos infrastructure . Stripe processing stablecoins at enterprise-scale is evidence that stablecoin payments aren't hypothetical. They're already running.

Layer 5: Distribution and Payout

Getting money into a stablecoin system is Layer 4. Getting it out is where the infrastructure gets stress-tested.

Platforms need to pay out in stablecoins, settle back to fiat over local rails, or both. The payout layer has to handle volume, support multiple corridors, and settle reliably every time. This is also where the "last mile" liquidity problem shows up: stablecoins have made real progress on the middle mile of cross-border payments, but liquidity between stablecoins and local fiat currencies remains thin in many corridors. Thin liquidity means slippage, delay, and unreliable pricing. For a platform promising its partners reliable settlement, that's an existential problem.

This is also where DIY stablecoin stacks most commonly break. A platform that built Layers 1 through 4 with four different vendors now discovers that none of them handle payouts in the corridors its partners need, or that settlement times are inconsistent because the payout provider's compliance model doesn't align with the custody provider's reconciliation cycle. The connective tissue fails before the money reaches the recipient.

Paxos powers stablecoin payouts and fiat settlement for programs running in production today. USD settlement and select corridors are handled directly through Paxos. For broader FX and local account delivery, Paxos works through partner integrations to extend reach without compromising regulatory standards.

Layer 6: Conversion (Fiat-Stablecoin Swap)

Conversion isn't a single event, it's a recurring operation that happens at multiple points in the payment flow. Fiat to stablecoin at funding. Stablecoin to stablecoin for treasury management. Stablecoin back to fiat at payout. Each conversion requires liquidity, asset access, and settlement infrastructure.

The stablecoin market is more competitive than ever, with multiple issuers and multiple tokens in active circulation. Platforms that try to build conversion relationships individually end up managing separate integrations with each issuer, each with its own settlement cycle and risk profile. That complexity multiplies with every new token and every new corridor. And as stablecoin commerce grows (consumer-to-business transactions more than doubled last year), the conversion layer becomes the throughput bottleneck for the entire stack.

Paxos provides conversion and orchestration across PYUSD, USDP, USDG, and USDC, with multi-venue liquidity strategies and unified orchestration APIs. USDT conversion is live for institutional customers in select jurisdictions, with broader availability in the coming months. A single integration replaces separate issuer relationships and gives partners access to institutional-grade pricing and execution.

The Bigger Picture

The six-layer model isn't just an infrastructure framework. It's a map of the regulatory and operational surface area that separates platforms that talk about stablecoin payments from platforms that actually process them.

The stakes extend beyond payments. Stablecoins are giving rise to a new form of banking-as-a-service: one built on on-chain infrastructure rather than rented bank licenses and legacy core systems. The payments layer is where the account gets opened. Credit, investing, and treasury products are where the business gets built. Every platform that solves the six-layer problem for payments is also building the foundation for the next generation of financial products.

But the inverse is equally true. Every platform that leaves gaps in its infrastructure, is building on a foundation that won't support what comes next. For example, a custody layer that doesn't connect to its compliance engine, a payout corridor that can't reconcile with its funding rails, a conversion layer that adds days of settlement latency is building on a foundation that won't support what comes next.

Paxos removes those gaps with infrastructure built and operated under active regulatory supervision, backed by over a decade of track record, SOC 1/2 Type II certification, and enterprise programs already running at scale. The question isn't whether stablecoin payments are coming to your platform. It's whether the infrastructure underneath them is ready for what they'll need to become.